The air cargo industry outlook for 2025 is positive following a busy December but the market also faces a range of risks, including an overreliance on e-commerce, according to analyst Xeneta.

These are two key market observations by Xeneta, whose chief airfreight officer, Niall van de Wouw said the airfreight market is increasingly reliant on e-commerce volumes, but there isn’t anything to plug the gap should e-commerce trade flounder.

He said: “We can put a ribbon around 2024. It was quite some year for air cargo. But this remains a market that is increasingly reliant on e-commerce volumes, while the general freight market, the bellwether of the global economy, remains muted. The signals from the manufacturing industry, particularly in Europe, are concerning but e-commerce continues to take up this slack and is projected to grow at +14% annually to 2026.

“So, the overall outlook for air cargo remains one of growth. But reports of countries aiming to crack down on the Chinese e-commerce platforms, for example, if this was to happen, would have a sizeable impact in markets around the world because what’s going to take the place of these volumes?”

Some stakeholders in the industry are of the view that e-commerce has become a saturated market, while various government regulations may restrict it regardless.

A number of market commentators have also questioned how much longer the airfreight industry will benefit from sea-air modal shift as a result of the Red Sea crisis.

On the subject of disruptions that benefit air cargo, Xeneta observed that the threat of strikes at US east coast ports did not result in a significant uplift for airfreight last month and now with an employment deal for workers at east coast US ports, the potential for air cargo to benefit is slim.

”Concerns about potential second-round strikes at US east coast ports failed to produce a meaningful mode shift to air freight in December and news on January 8 of a tentative agreement between the International Longshoremen’s Association (ILA) and United States Maritime Alliance (USMX) for a new six-year Master Contract means any further boost to air cargo volumes as a result of East Coast ports disruption is now far less likely.”

That said, the analyst added there may be business opportunities born out of other potential ocean freight issues.

”While the threat of further US east coast port strikes seems to have now been removed, any further disruptions to global ocean freight is likely to see shippers resorting to the predictability of airfreight for urgent shipments, triggering further spikes in air cargo rates. October’s three-day strike at US ports produced a 12% jump in air cargo volumes month-on-month from Europe to the US,” said Xeneta.

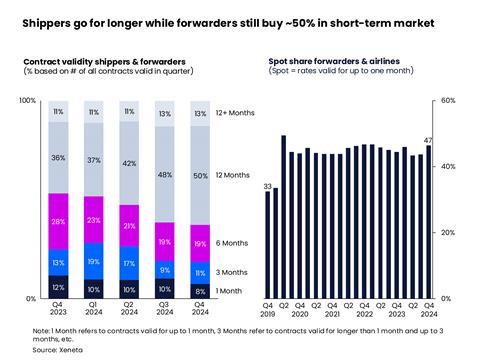

Another hot topic in the industry has been the drive to secure capacity to avoid high spot rates, which Xeneta encouraged shippers and forwarders to do last summer ahead of the fourth quarter peak. But according to Xeneta’s data, some forwarders were still shelling out for capacity at short notice last year.

“Historical trends indicate that, in 2024, shippers demonstrated a growing preference for longer term airfreight contracts, with durations of one year or more,” stated Xeneta. “These contracts accounted for 63% of all agreements valid in Q4 2024, marking a 16-percentage point increase compared to the same period in 2023.”

“Meanwhile, during this timeframe, freight forwarders continued to negotiate nearly half of their volumes in the spot market, a strategy that likely has eroded their revenues due to rising airline selling rates.”

Spotlight on spot rates

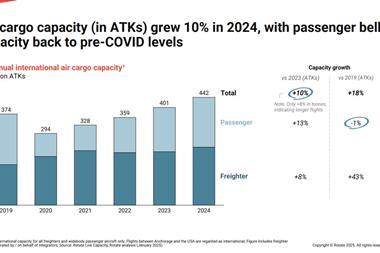

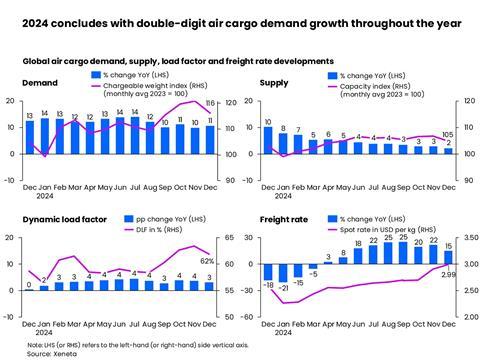

Average global spot rates finished the year 15% higher year on year, but there was more market maturity with pre-peak strategic capacity allocation by airlines, securing of capacity by freight forwarders and longer term contracts by shippers. All of this resulted in moderate spot rate increases compared with 2023.

The December global air cargo spot rate increased 15% year on year to $2.99 per kg, although the comparison with the high-rate level in December 2023 made this the slowest growth rate in the last seven months, said Xeneta.

As projected by the analyst, the 2024 year-end peak season concluded with a more moderate spot rate increase of 11% between September and December. In the corresponding period of 2023, there was a 21% surge in spot rates.

December saw the Europe-to-North America air spot rate experience the most significant month-on-month increase, rising 21% to $3.27 per kg, its highest level in over two years. This spike is likely due to reduced cargo capacity from airline winter schedules on passenger flights and the reallocation of freighter capacity to Asia, said Xeneta.

As of early January, Europe to the US spot rates stood at $2.56 per kg, a 25% drop from their peak two weeks earlier.

In comparison, the Northeast Asia-to-North America corridor saw a month-on-month increase of 5% in December, reaching $5.57 per kg. Close behind, the Northeast Asia-to-Europe market posted a 4% rise, bringing rates to $5.28 per kg.

The spot rate on the China-to-US corridor, unlike other key lanes, showed a decline of 9% from its mid-December 2024 peak of $5.61 per kg to early January 2025. This contrasted sharply with the same period in 2023, when rates dropped nearly 40% from a peak of $5.91 per kg.

Changes to the e-commerce sector played a part here, said Xeneta.

“A combination of strategic allocation of cargo capacity and tightened scrutiny on e-commerce activities may have contributed to subdued peak season levels, while concerns over potential Trump tariffs likely tempered the rate decline due to increased frontloading.”

While IATA predicted that air cargo volumes would rise by 5.8% year on year in 2025, Xeneta offers a prediction of 4-6% growth in global air cargo demand, continuing to outpace global cargo capacity supply growth of 3-4%.

But air cargo stakeholders remain cautious, Xeneta stated. Industry challenges include a subdued manufacturing outlook, geopolitical tensions, threats of Trump tariffs, tightened measures of de minimis threshold related to e-commerce, increased security risks from rising global tension and extreme weather and natural disasters.

“Heightened market volatility due to rising global uncertainties will continue to impact air cargo demand and this could force air freight rates to fluctuate significantly,” said van de Wouw.

“Therefore, embracing more flexible freight rate negotiation methods, such as indexing or transparent pricing, could foster mutual understanding and better collaboration across the industry this year.”