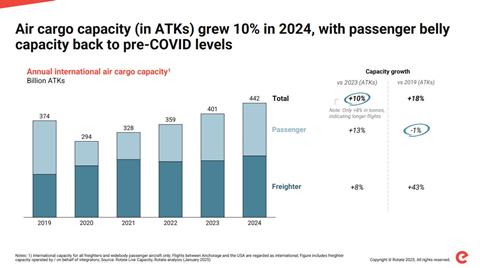

Air cargo capacity grew by double-digit percentage levels last year, with bellyhold capacity continuing to recover and freighter space remaining above pre-Covid levels.

Figures from data provider and consultant Rotate show that in 2024 total air cargo capacity in airfreight tonne km terms (ATK) was up 10% year on year to 442bn ATK.

The increase was led by the return of passenger services as bellyhold capacity increased 13% year on year and is now just 1% behind pre-Covid 2019 levels.

Meanwhile, freighter capacity was up 8% year on year in 2024 as the industry continues to rely on all-cargo aircraft more than it did in the past.

Compared with pre-Covid 2019 levels, freighter capacity is up 43%.

Rotate pointed out that while capacity is up 10% year on year in ATK terms, it has increased by the lower amount of 8% in tonnage terms – indicating that part of the reason for the larger increase in ATK terms is that aircraft are flying longer distances as well as carrying more cargo.

The largest increases in capacity are rather unsurprisingly on the main east-west trades out of Asia, where e-commerce demand fuelled rapid demand growth in 2024.

Rotate figures show that headhaul ATK capacity from Asia Pacific to North America increased by 15% last year.

Meanwhile, from Asia to Europe there was a 16% increase in ATKs.

From Asia to the Middle East there was a 17% increase and from the Middle East to Europe space was up 15%, reflecting modal shift from sea to air due to the Red Sea missile crisis as well as general e-commerce fuelled market growth.

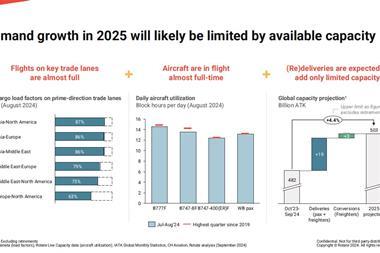

Looking ahead, it is expected that it will be hard for the air cargo market to continue growing at the same pace.

Speaking at the Tiaca Air Cargo Forum last year, Rotate chief executive Ryan Keyrouse highlighted some of the issues the industry could face on the supply side.

He pointed out that belly capacity growth is slowing down, there are delays to aircraft production and the high demand being experienced on the passenger side of the market was affecting the amount of feedstock that is available to be converted into cargo aircraft.

Keyrouse said that aircraft utilisation was at its highest level in the past five years meaning it was unlikely that more capacity could be squeezed out of the current global fleet.

“We are almost at maximum utilisation so the aircraft can’t fly more and [in 2025] we see a maximum of 4.4% capacity growth, if you look at deliveries and conversions,” Keyrouse said.

“We haven’t factored in retirements so it will only be lower if we retire a few aircraft.

“If you have a 4.4% capacity growth and a 20% demand growth [from China], it can only come from one place - moving capacity from Africa and Latin America into these markets.

“You have to wonder how far can that go, but that is really only the lever that you have for increasing capacity for this demand.”