Source: Natalya Kosarevich/Shutterstock.com

The results from the latest Air Cargo News industry outlook survey are in and respondents are feeling positive despite some real concerns.

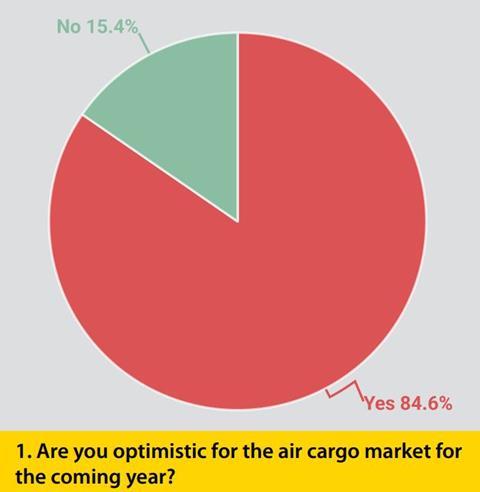

The air cargo industry is optimistic for the year ahead with volumes expected to increase despite concerns about rising protectionism and conflicts, according to the latest Air Cargo News industry outlook survey.

The annual survey was carried out in January and almost 100 airfreight professionals responded, with 84.6% saying they were optimistic for the year ahead, an improvement on the 70% recorded in 2024.

Respondents said they expected lower interest rates, lower inflation and a return of consumer confidence to support demand levels. Others said that ongoing e-commerce demand and peace treaties in conflict zones could support demand levels.

Another remarked that a reversal of green policies could boost the automotive and oil and gas sectors, while the semiconductor and pharma markets were other areas of potential growth identified by respondents.

However, the unpredictability that currently surrounds the market was also acknowledged. “I think [US president] Donald Trump’s planned increase of tariffs on imports to the US, especially from China, could dramatically impact the volumes of e-commerce traffic that are currently bolstering the airfreight market,” said one respondent.

The overall consensus was that improved consumer spending due to lower inflation and e-commerce demand growth should be enough to offset the declines caused by a rise in protectionism.

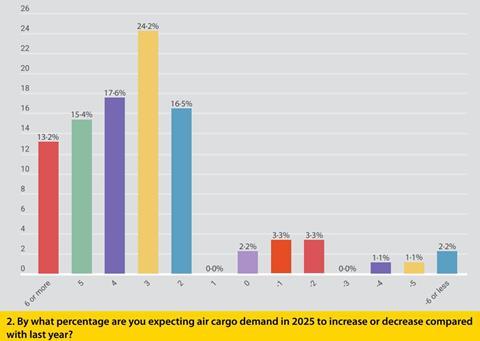

The survey also asked how much the air cargo market is expected to grow or decline in percentage terms in 2025.

Just over 24% of people said they expected the market to grow by 3% year on year, followed by an increase of 4% and then a 2% improvement. Very few people said they expected the market to decline in 2025, reflecting the optimism for the coming year expressed in the first question.

One respondent said that demand levels would be supported by increasing air capacity between North America and Asia – a trade lane that has suffered in recent years due to the slow restart of passenger operations.

Others pointed to expectations that global GDP is expected to increase by 2.8% this year and the market would improve in line with that.

One respondent, who expected a 2% increase, was concerned about the potential impact of tariffs on the e-commerce market. Another pointed out that the lack of elections in major economies – unlike last year – should support business investment. There could also be a benefit from post-war reconstruction efforts, another remarked.

The less optimistic, those who expected a large decrease of 5% or 6%, were largely concerned about the potential impact of a trade war on the global economy.

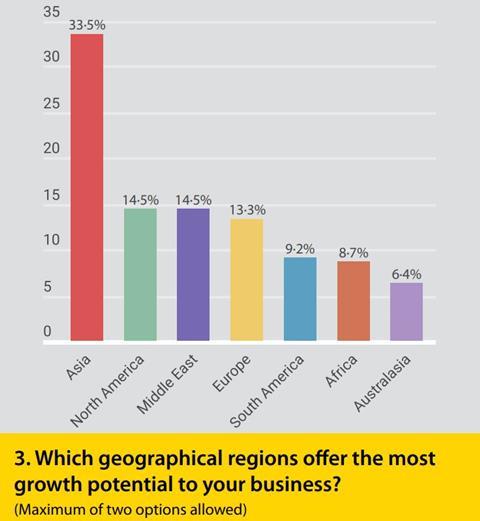

Growth potential

The next couple of questions focussed on where growth in the market could potentially come from, with respondents asked to select a maximum of two choices.

Regionally, and perhaps unsurprisingly, Asia was by far the region people felt most likely to generate growth, attracting 33.5% of responses. North America and the Middle East were tied in second place, just ahead of Europe.

One respondent remarked that within Asia, India and Southeast Asia were two markets to watch due to growing economies and the development of China+1 manufacturing.

In the Middle East, growth is expected to be fuelled by infrastructure projects and the need to rebuild after conflicts in the region, respondents said.

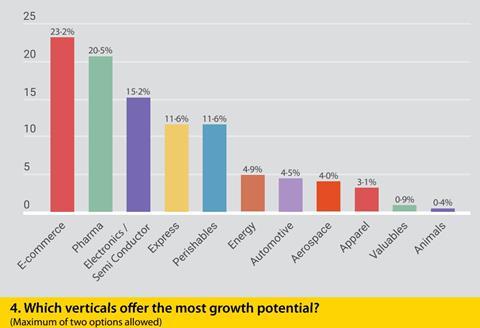

Looking at which verticals would grow the most, there were again no surprises with e-commerce taking 23.2% of the vote, ahead of pharma with 20.5% and then electronics/semi-conductors on 15.2% – two options could be chosen for this question.

Perhaps the biggest surprise here was how close pharma came to e-commerce. One respondent pointed out that as the use of personalised genetic medicine increases, the demand for quicker turnaround of smaller pharma packages will grow.

Express and perishables also performed well, both attracting 11.6% of the vote.

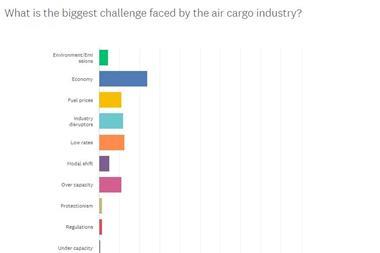

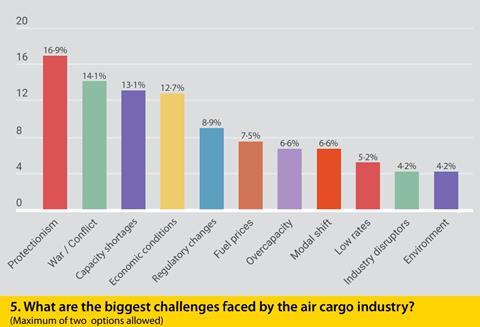

On the biggest challenges facing air cargo, a question where two answers could be selected, protectionism with 16.9% and conflict on 14.1% were the biggest concerns, ahead of capacity shortages on 13.1% and economic conditions on 12.7%.

On capacity shortages, one person remarked that the e-commerce boom has resulted in “regular” capacity shrinking as airlines dedicate capacity and ACMI operations to e-commerce.Another said the reduction in passenger flights was limiting the availability of bellyhold space.

“Global supply chain bottlenecks and geopolitical tensions also impact the smooth flow of goods,” said another.

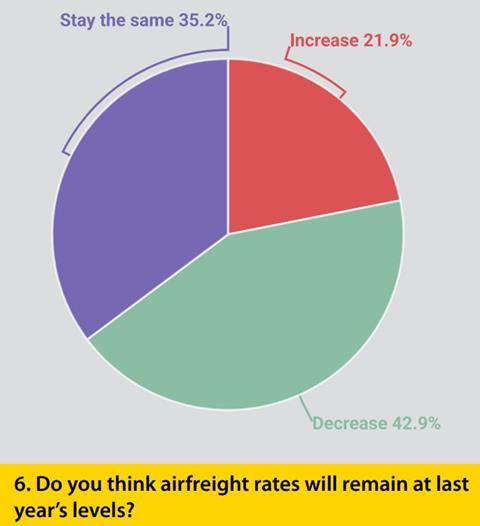

Rate expectations

Meanwhile, on the topic of how airfreight rates will progress this year, most said they expected them to remain flat, followed by expectations of a decrease and finally an increase. This is perhaps as much a reflection of the high rates recorded last year as expectations related to the supply/demand balance.

Those expecting rates to remain the same said this would be the result of a market stabilisation this year, while those expecting an increase were pessimistic about the outlook for air cargo given the potential impact of tariffs and protectionism on trade and e-commerce. With Suez Canal shipping potentially restarting, a shift back to ocean from air was also mentioned.

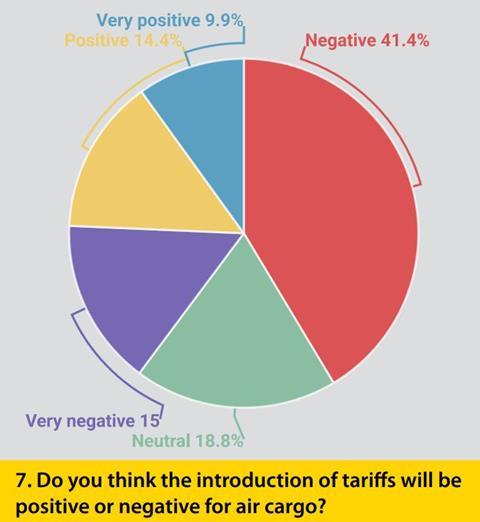

Asked about the impact of tariffs on the market, most said it would have a negative impact.

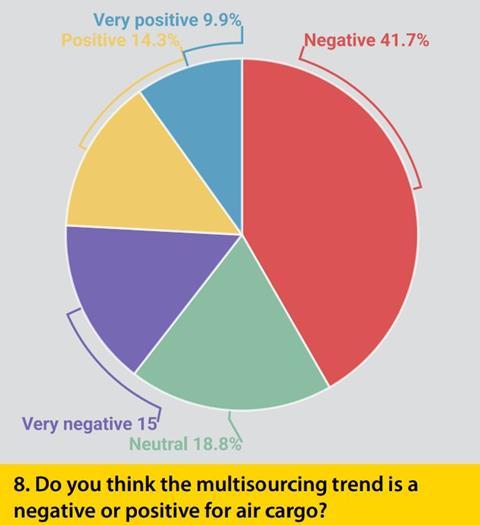

Meanwhile, multisourcing was seen as a positive development for the market.

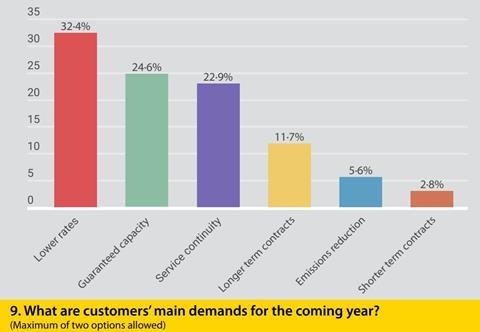

The next question focused on what is most important to customers at the moment, with the option to select two choices. This year, lower rates once again topped the list for 32.4% of respondents, ahead of guaranteed capacity and service continuity.

“Looking ahead, airfreight and logistics customers will have specific expectations, influenced by current market trends, global challenges and evolving industry needs,” explained one respondent.

“Customers prioritise reliability and sustainability to meet operational needs and regulatory pressures,” remarked another.

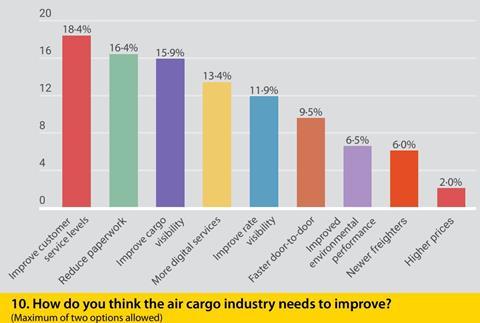

Service level boost

The survey also considered how the industry should improve, with two options allowed. Service levels came top for the second year with 18.4%, just ahead of reduced paperwork (16.4%) and improved cargo visibility (15.9%).

“Enhanced transparency builds customer trust, while greener solutions align with environmental priorities,” said one respondent.

“In India, there is no yardstick determined for improving customer service levels for the service providers in the processing and movement of cargo, which is very important for the improvement of services continuously,” said another.

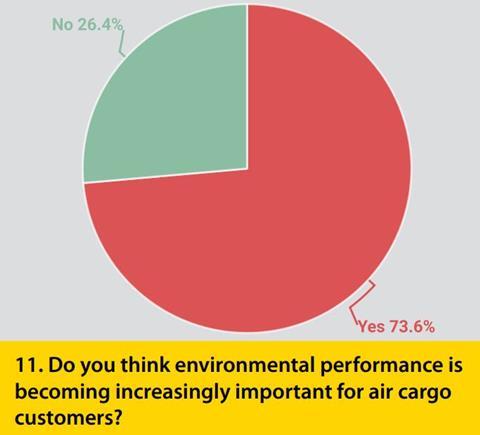

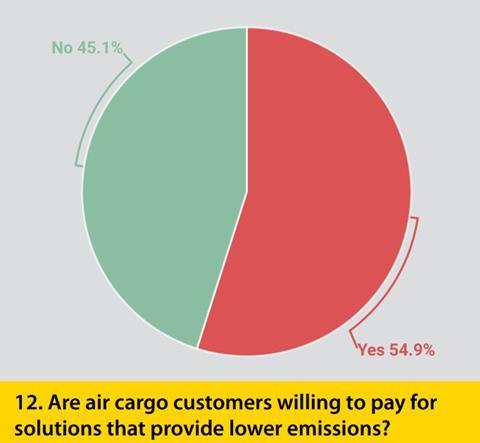

The final two questions of the survey looked at sustainability. The first asked whether environmental requirements are becoming more important for customers, with 73.6% saying they are – an increase on last year’s 66.4%. Yet, 54.9% of respondents said that customers were not willing to pay more for solutions that provide lower emissions.

Customers are willing to invest in sustainable options if it aligns with their environmental goals and regulations, remarked one respondent.

Another added: “Yes, more and more air cargo customers are willing to pay for solutions that reduce emissions, but this willingness depends on several factors, such as the sector of activity, the environmental sensitivity of the customer and the economic context.”

Another said prices were already high, making it difficult to secure more for sustainable solutions.